- Solutions

-

-

Featured Solution

Get more value from your existing SAP BW and SAP HANA investments with our SAP integrations.

Get more value from your existing SAP BW and SAP HANA investments with our SAP integrations.

-

-

Forecasting is an indispensable requirement for any modern organization looking to gain a competitive edge. To do it well, today’s companies need the flexibility to adjust algorithms and define their own criteria to best suit their particular business needs. However, many business intelligence tools limit users’ ability to fine-tune forecasting algorithms.

Pyramid provides out-of-the-box forecasting that can be performed with a single click. More advanced manipulations of parameters can be achieved using Pyramid’s advanced forecasting dialog. And when a user has a specific forecasting requirement, he or she can deploy custom scripts to achieve this.

In a previous blog, I demonstrated how Pyramid had made Python (and R) a first-class citizen in its architecture and product strategy, using a stock market example to highlight this. In this blog, I will demonstrate how Python (and R) scripts can be used to meet customized forecasting requirements.

Janice is a data scientist for R&G Distributors. R&G uses Oracle as a data warehouse and Pyramid for data visualization, reporting, and analytics.

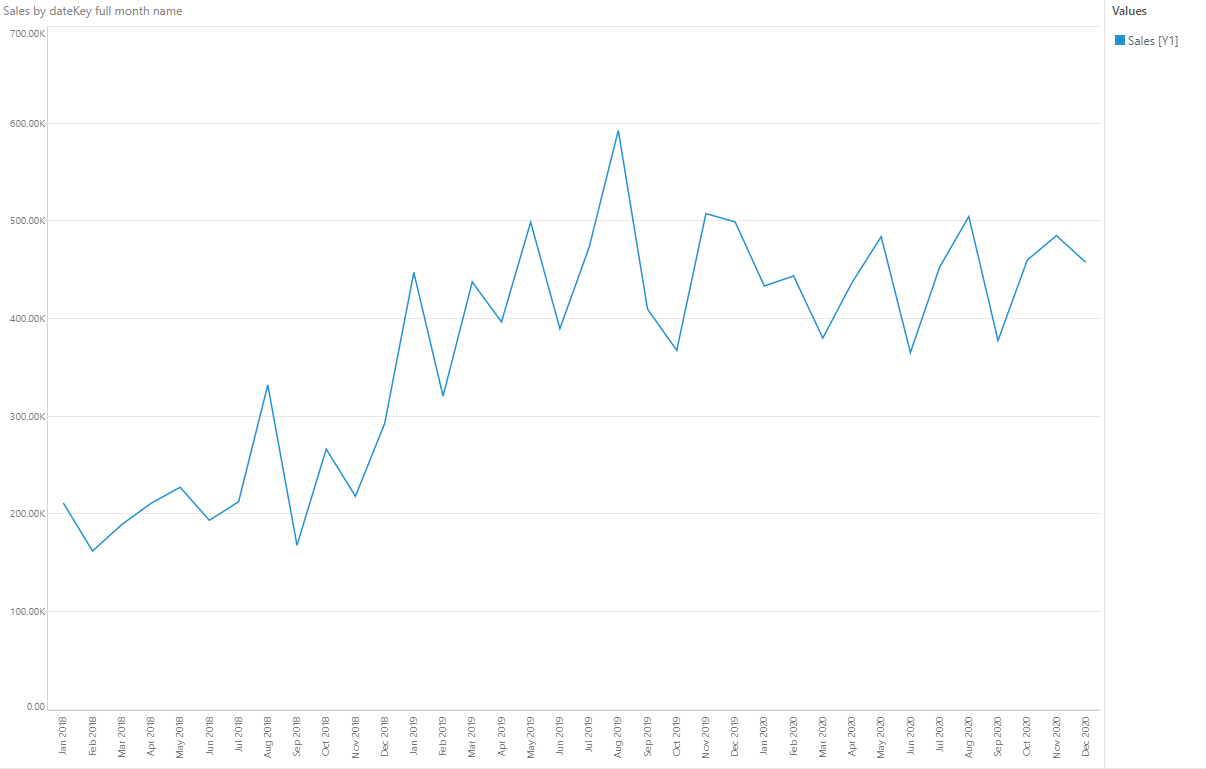

Janice wants to apply a forecasting algorithm that calculates forecasted values based on previous averages. Using Pyramid, Janice creates a graph depicting sales for the last three years.

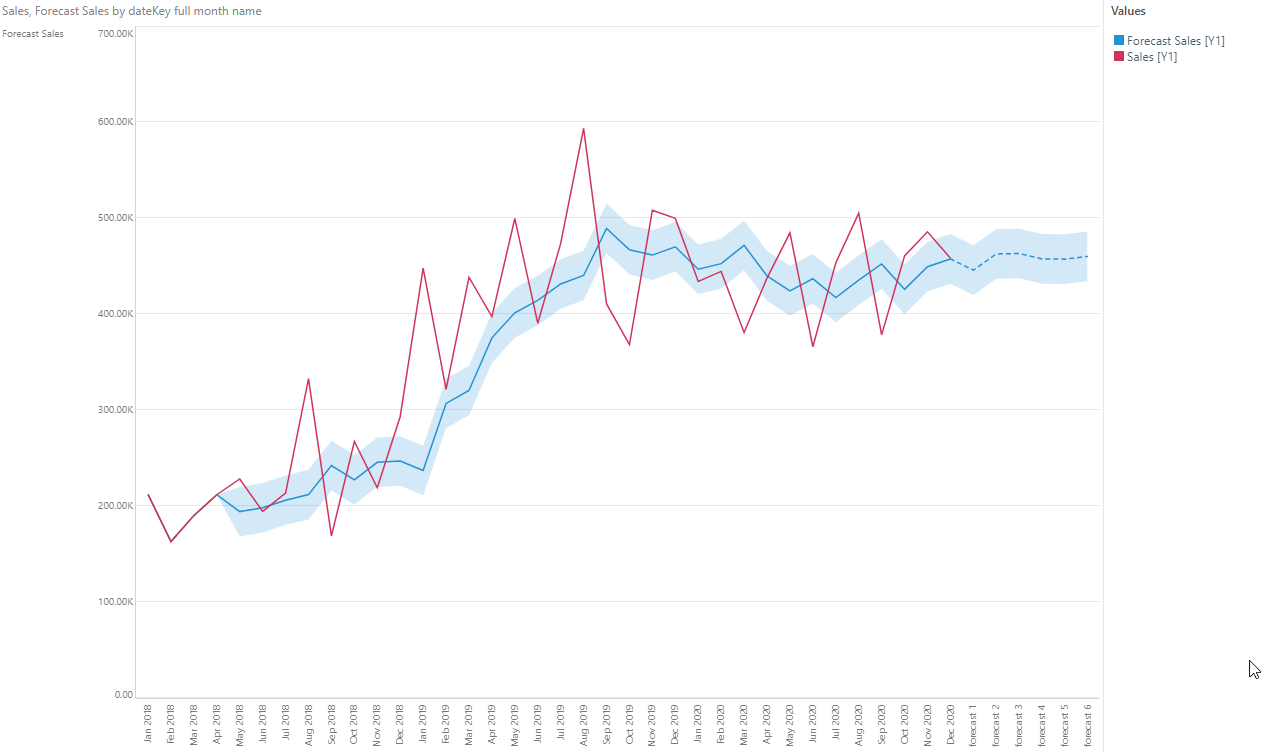

From her Discover report, Janice applies her own Python script that forecasts sales based on previous averages.

import scipy.stats as st

import pandas

def pyramid_forecast(dataLst, period, futures, shouldCalcHistory):

if period == 0:

period = 6

size = len(dataLst)

movingAvgs = []

if size < period+1:

return pandas.DataFrame({'forecast': []})

if shouldCalcHistory:

startIdx = period-1

for i in range(startIdx, size-1):

sum=0

for j in range(0,period):

sum += dataLst[i-j]

movingAvgs.append(sum/period)

# Future predictions. First

for i in range(0,futures):

sum = 0

# take the last element of the data into the some

elementsToTakeFromData = period-i

for j in range(size-elementsToTakeFromData, size):

sum += dataLst[j]

if elementsToTakeFromData < 0:

elementsToTakeFromData=0

# take the rest of the elements from the moving avgs itself (includes predictions)

elementsToTakeFromPredictions = period-elementsToTakeFromData

for j in range(len(movingAvgs)-elementsToTakeFromPredictions, len(movingAvgs)):

sum += movingAvgs[j]

movingAvgs.append(sum/period)

interval1High = []

interval1Low = []

interval2High = []

interval2Low = []

startIdx = 0

if not shouldCalcHistory:

startIdx = len(movingAvgs)-futures

for i in range(startIdx, len(movingAvgs)):

x = movingAvgs[i]

currInterval1 = st.t.interval(0.95, len(dataLst) - 1, loc=x, scale=st.sem(dataLst))

currInterval2 = st.t.interval(0.95, len(dataLst) - 1, loc=x, scale=st.sem(dataLst))

interval1Low.append(currInterval1[0])

interval1High.append(currInterval1[1])

interval2Low.append(currInterval2[0])

interval2High.append(currInterval2[1])

df = pandas.DataFrame({'forecast': movingAvgs[startIdx:len(movingAvgs)],

'interval1High': interval1High,

'interval1Low': interval1Low,

'interval2High': interval2High,

'interval2Low': interval2Low})

return df

Janice then applies the script to her report and selects historical forecasting to view the accuracy on historical data.

Janice then tweaks the algorithm by changing the previous periods from four to six, and increases the accuracy to ninety-five percent. The newly adjusted forecast is displayed automatically after she applies the changes.

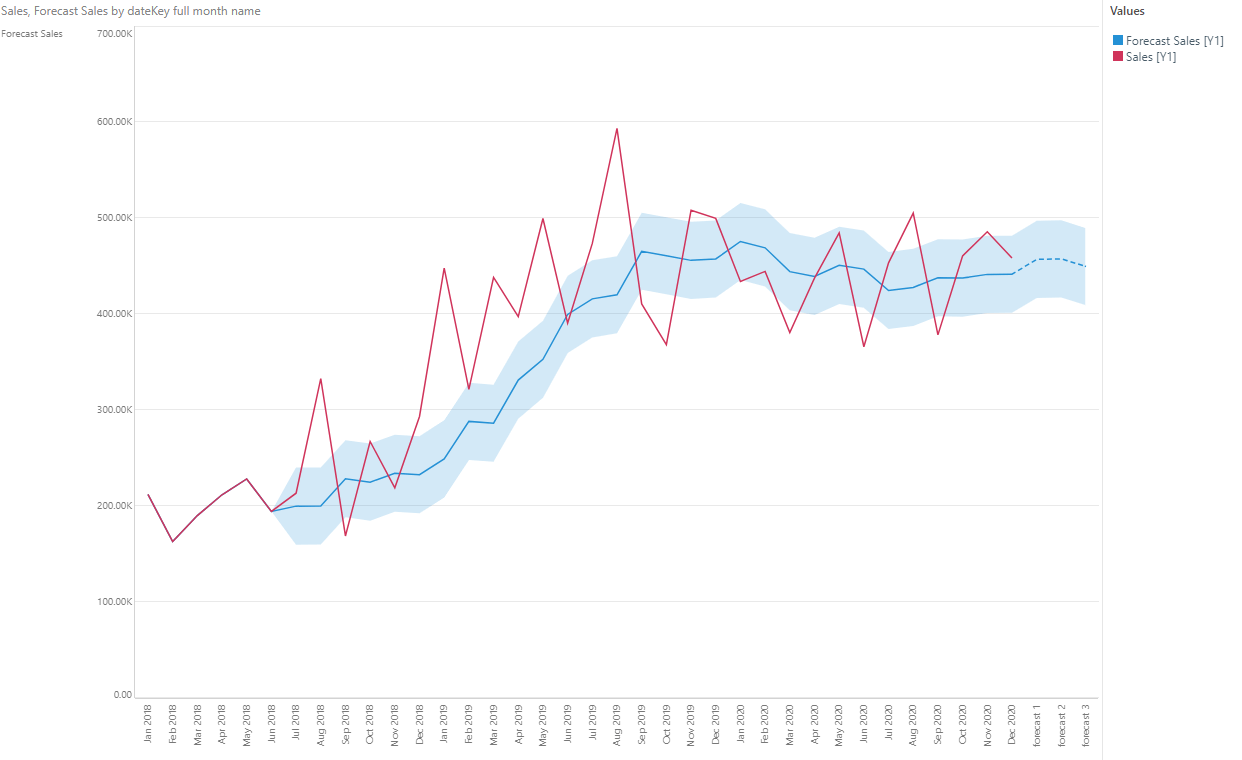

Janice can then save the adjusted script to ensure it will be available in other reports and dashboards. Janice could optionally introduce additional input factors to the Python script to further modify and enhance the script and view the desired forecast.

Pyramid provides multiple forecasting algorithms that can be executed with a single click, as well as an advanced forecasting dialog, where options can be tweaked for improved performance. Most third-party BI tool vendors only offer a standard forecasting method where users have limited ability to adjust the algorithm, with no option to write their own code.

However, data scientists need to be able to deploy customized Python and R forecasting scripts. With Pyramid, they can create and share their own scripts in a governed content management platform. Scripts can also be configured to run with specific package versions using specific Python or R versions in a virtual Python environment. Pyramid also provides a marketplace with free reusable Python source code with a library of predefined forecasting functions.

How-To

SAP is essential enterprise software. Your organization has made significant investments in SAP. You've tailored…

How-To

Pyramid’s built-in multi-factor authentication (MFA) option adds a rock-solid layer of security to your BI…

How-To

Administrators occasionally need to check complicated settings and security structures for users. Sometimes the easiest…

How-To

Pyramid lets users customize and personalize the labels of value metrics and hierarchies for a…

How-To

Static data format masks, used to format values in analytics) is a standard feature in…

How-To

Pyramid lets users display multiple value metrics in a single report, each with its own…

How-To

Pyramid’s persistent color feature maintains the same color in all visualizations for selected data elements,…

How-To

Pyramid offers flexible, intuitive security for parent-child hierarchies, providing role-based control over how members are viewed…

How-To

Pyramid excels in its’ native support for parent-child hierarchies, automatically generating hierarchical structures and providing fluid,…